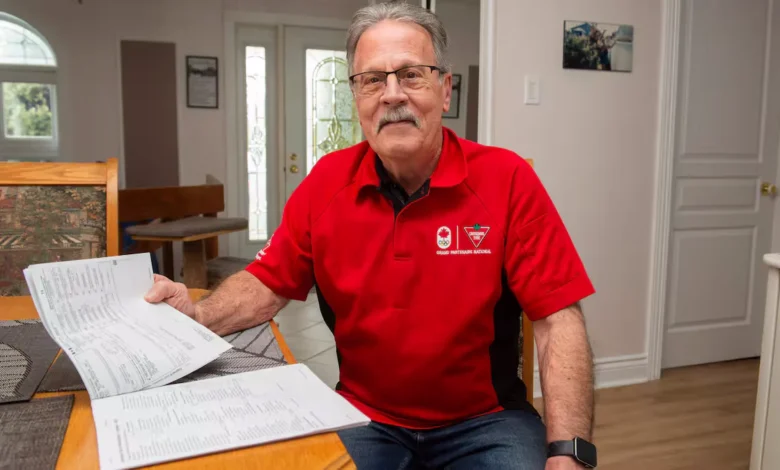

Many retirees face the dilemma of continuing to work after retirement, particularly due to tax burdens. Michel Pelletier, a 67-year-old retiree from Mont-Saint-Hilaire, shares his frustrations about this issue. After serving as a senior account manager at the Bank of Montreal, he now works part-time at Canadian Tire, hoping to maintain social connections and stay active.

Concerns Over Taxation for Retirees

Despite the benefits of working, Pelletier finds the tax implications disheartening. He makes about twelve hours a week at Canadian Tire, but he worries that the extra income leads to excessive taxation. “It seems pointless because I end up giving so much to taxes,” he lamented.

Efforts to Minimize Tax Impact

In an attempt to lessen his tax burden, Pelletier has opted for higher withholding on his paycheck. Additionally, he continues to contribute $4,500 annually to his Registered Retirement Savings Plan (RRSP) without withdrawing any funds. He believed that this strategy would mitigate his financial discomfort.

Pelletier’s situation worsened with recent changes to Quebec’s career extension tax credits. Previously, he received a tax credit of $1,500; this has now reduced to just $400. “That’s a significant decrease,” he noted, expressing concern about how future withdrawals from his RRSP will affect his finances.

The Financial Reality of Working After Retirement

From a financial standpoint, continuing to work post-retirement may not always be beneficial. The potential for moving into a higher tax bracket exists, leading to more taxes owed on any additional income. Moreover, certain government benefits are also reduced as income rises.

Implications for Government Benefits

- The Old Age Security Pension is decreased if net income exceeds $93,454 (2025).

- The Guaranteed Income Supplement is entirely eliminated for individuals with net incomes over $22,512.

Fortunately, the benefits from the Quebec Pension Plan (QPP) remain unaffected regardless of earned income. This aspect offers some relief to those choosing to supplement their retirement income by working.

Retirees like Pelletier urge the government to reconsider policies that affect older workers. “It would be great to have support for seniors who want to work without being overwhelmed by taxes,” he suggested.

The conversation around working after retirement continues to spark discussions on fair treatment and financial viability for seniors. As more individuals navigate this landscape, the emphasis on supportive policies becomes increasingly essential.