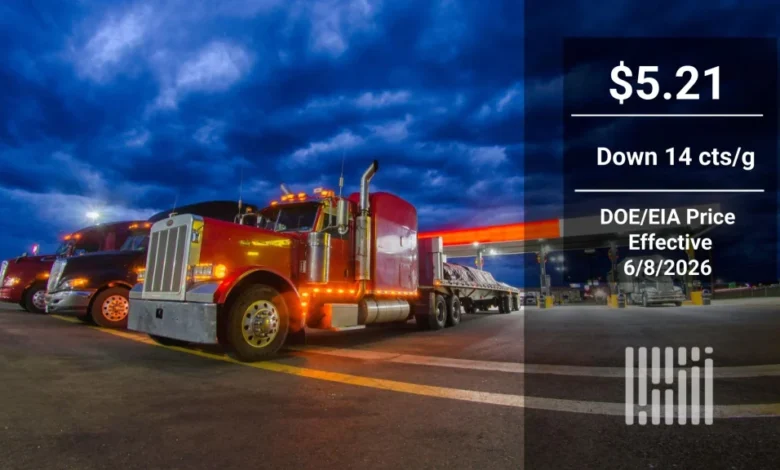

Diesel prices are experiencing a notable downward trend, evidenced by recent reports indicating a benchmark price of $5.21 per gallon. This rate marks the lowest since military hostilities with Iran began in March, exemplifying a critical inflection point for the oil market. Over the past five weeks, diesel prices have decreased by 43 cents per gallon, prompting analysis about the disconnect between the Department of Energy/Energy Information Administration (DOE/EIA) prices and the AAA daily average of $5.317 per gallon.

Understanding the Disconnect in Diesel Pricing

This persistent decline occurs amidst falling futures prices, yet conversations around “tank bottoms” are growing louder. These “tank bottoms” refer to a drastic depletion of global inventories, which would minimally sustain the petroleum distribution system. John Arnold, a respected trader, voiced his surprise at the market’s resilience after 100 days of the Strait’s closure, indicating that complacency may not be justified given the lack of clarity on reopening.

According to the latest EIA report, total U.S. crude inventories have plummeted to 1.573 billion barrels— the lowest level observed in over two years, marking a continued decline for ten consecutive weeks. This statistic is pivotal, given that the United States remains the world’s largest consumer of oil. As such, the data is closely scrutinized for signs of larger shifts in global market dynamics.

| Stakeholder | Before Price Drop | After Price Drop | Impact |

|---|---|---|---|

| Consumers | $5.64/gallon | $5.21/gallon | Lower transportation costs |

| Oil Companies | High inventory levels | Low inventory levels | Pressure to cut production |

| Traders | Future profits projected | Risk of losses from backwardation | Uncertainty in investment decisions |

| Government Regulators | Stable market | Potential for export bans | Increased regulatory scrutiny |

Market Signals: Supply and Demand Conundrums

Jeffrey Currie, a prominent voice in commodity trading, emphasizes that the physical markets reflect a disconnection from the paper markets, which appear to be trending bearish. The Brent crude market has fallen below $90 per barrel, yet prices in certain regions exceed $150. Currie elucidates that the supply shock mirrors the demand shock seen during COVID-19, highlighting the fragility of global supply chains. His assertion suggests that current futures prices are undervalued compared to physical market demands.

Despite these conditions, traders are not purchasing forward barrels to lock in anticipated higher future prices. The forward curve shows a unique backwardation structure, where immediate prices exceed future ones. Philip Verleger, an energy economist, points out that firms may hesitate to hedge against future prices since this may enforce immediate losses, often too significant for companies to absorb.

The Export Ban Worry: A Brewing Market Storm

Further complicating the situation, fears of a potential U.S. ban on crude and product exports loom large. If the current price trend reverses, such a ban could precipitate severe market disturbances, dramatically reducing oil values. In this climate of uncertainty, U.S. firms are incentivized to minimize their inventory to safeguard against unanticipated regulatory changes, reinforcing market volatility.

Localized Ripple Effects: Global Implications

This decline in diesel pricing resonates well beyond U.S. borders, reverberating across key markets in the UK, Canada, and Australia. Consumers in these regions could see gradual reductions in transportation and logistics costs, while oil-dependent economies may find themselves in a precarious position concerning production and regulatory strategies. The overall global economy could face unpredictable shifts as stakeholder reactions to lower inventory levels evolve.

Projected Outcomes: Navigating the Future

Looking forward, stakeholders should monitor three primary developments:

- Inventory Dynamics: Watch for changes in U.S. diesel inventories, as continuous drops may prompt heightened market reaction and regulatory scrutiny.

- Policy Shifts: The potential for U.S. export bans remains a significant risk. Tracked legislative developments could indicate market stability or volatility.

- Market Corrections: If global demand rebounds dramatically, pricing structures could shift toward contango, influencing trader behavior and company inventories.

In this intricate dance of supply and demand, stakeholders must remain agile, steered by evolving information and market dynamics. The current downward trend in diesel prices, while presenting short-term relief, hints at longer-term complications that could redefine the oil landscape.